When a Naturist Place Becomes Collateral

European Camping Group | Paribas Affaires Industrielles | Abu Dhabi Investment Authority

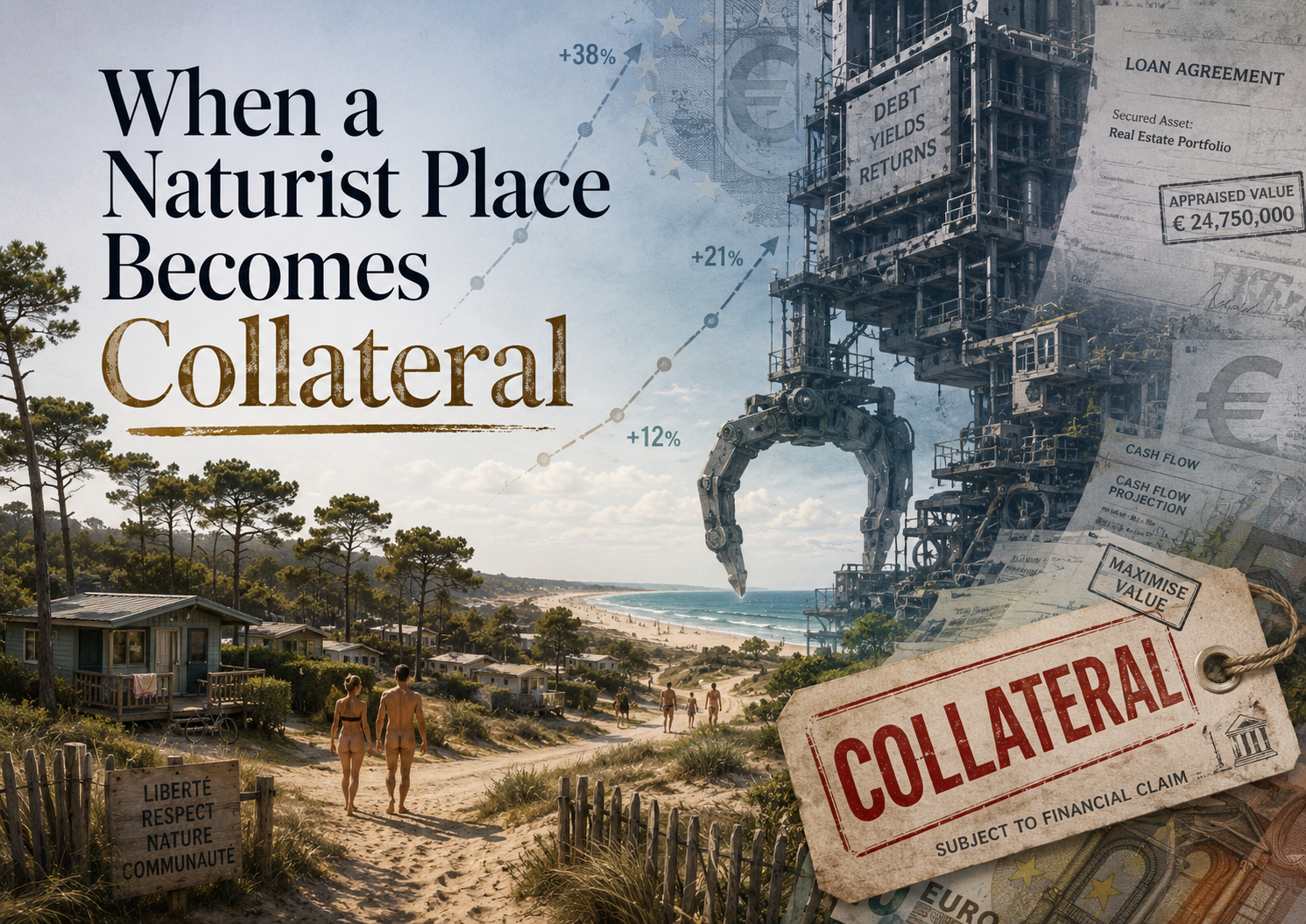

… debt, valuation …

CHM de Montalivet is not merely a commercial campsite but a historic phenomenon, social landscape and part of naturist cultural history. It represents family life, freedom, summer ritual, body acceptance, ecological proximity and post-war social experimentation amongst other things.

In eyes of Private Equity, such places may be seen differently.

A site like CHM may be targeted by one-eyed trouser snakes not because of its cultural meaning, but because it can generate recurring cash from holidaymakers, bungalow owners, mobile-home users, residents, services, rents, charges and seasonal visitors. The deeper question is what kind of success is being measured, and who benefits from it.

In March 2025, PAI Partners — historically rooted in Paribas Affaires Industrielles — announced selling a stake in European Camping Group to a subsidiary of Abu Dhabi Investment Authority. PAI described ECG as a “European leader in outdoor accommodation”. Le Monde reported that ADIA took a 40% stake and that ECG was valued at around €2 billion.

At first glance, that sounds like a success story: a large outdoor-accommodation group, international investors, growth, consolidation and confidence in the future of mobile-home holidays?

Another public fact gives the story a different tone. In February 2026, S&P Global Ratings published a regulatory notice stating that ECG Topco SAS planned to issue a €950 million Term Loan B, and assigned a preliminary ‘B’ rating. S&P’s formal language is more restrained, but the practical meaning is clear enough: this is speculative-grade debt, dependent on continuing cash generation and vulnerable to adverse conditions. In less polite language, one might say: highly polished debt with a faint smell of compost.

This is not necessarily a contradiction. A business can be valued highly by equity investors while also being viewed by credit analysts as a leveraged, speculative-grade borrower. That may be a private-equity split-screen: same group marketed as a valuable growth platform while also carrying an enormous debt that requires continued cash generation.

The public-interest question is therefore not simply whether European Camping Group is “successful”. This matters because cash generated at CHM could theoretically be used in very different ways. It could support resident protection, ecological stewardship, cultural preservation, transparent site maintenance, naturist education, public-interest governance, long-term reinvestment etc. Or it could be indirectly absorbed into group-level finance costs, acquisition debt, management charges, dividends, refinancing structures and investor returns.

At issue is whether a historic naturist place is best treated as a cash-producing asset inside a pirate-equity structure. Transparency is essential and urgent. Discussions about future of CHM de Montalivet should consider the extractive financial engineering above SocNat SA and European Camping Group.